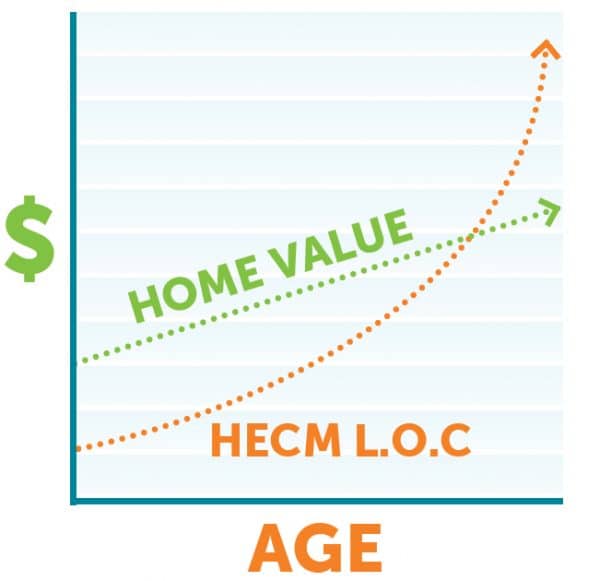

Your financial advisor may encourage you to have a line of credit for unexpected (or planned) purchases or shortfalls in cash flow. However, a HECM reverse mortgage has a clear-cut advantage over the traditional credit line, in that it has a growth option (growth applies to unused funds).

While the cost of setup for a HECM is higher, the advantages may outweigh the costs, depending on your situation. The unused funds in your line are guaranteed to grow regardless of the general economy, interest rates, or the underlying value of your home. If you take out a HECM at age 62 instead of 82 and leave the funds to grow instead of using them, it’s possible that the credit line could grow to be greater than the value of your home, especially in areas of the country home where values don’t increase substantially.*

The earlier you set up your line of credit but don’t use the funds, the more growth in the credit line would occur. You could potentially have a substantial credit line available in your later years when you may need it the most.

Even though your cash flow and your investments may be fine now, 20 to 30 years of retirement is a long time, which is why it’s prudent to ensure that a portion of your home equity, an important part of your nest egg, is readily available in cash without having to sell your home. You can draw out that home equity and still live in your home by only paying your basic home expenses, such as taxes and insurance, and maintaining the home. This is an example of having your cake and eating it too!

Most common uses of a reverse mortgage when you don’t need the money now:

- Use as a standby line of credit.

- Bridge the Medicare gap from 62-65

- Pay for life insurance

- No mortgage payments other than taxes, insurance and maintaining the home*

- Loan proceeds are tax-free which means all your investments may last longer.*

- Purchase a second home

Everyone has a different situation, sets of needs, wants and challenges. It will be well worth your time to meet with one of our reverse mortgage planners to receive a personalized, no-obligation consultation to see if a reverse mortgage is right for you.